In the rapidly evolving digital economy, payment gateways serve as the critical bridge between a merchant’s website and the financial institutions that handle customer payments. As online commerce has surged, so has the demand for secure, seamless, and developer-friendly payment gateway integrations. This comprehensive guide delves into how payment gateways work, how developers can integrate them, and best practices for ensuring security.

This article covers everything you need to know as a developer, from understanding the payment gateway architecture to exploring APIs, implementing front-end and back-end solutions, ensuring PCI compliance, and protecting customer data. Let’s start by understanding the basics.

1. What is a Payment Gateway?

1.1 Definition

A payment gateway is a service that authorizes and processes payments for e-commerce websites and brick-and-mortar stores. It acts as an intermediary between the customer and the merchant, securely transmitting payment information.

1.2 Role in the Payment Ecosystem

- Merchant: The business selling a product or service.

- Customer: The individual making a purchase.

- Issuing Bank: The customer’s bank.

- Acquiring Bank: The merchant’s bank.

- Payment Processor: Handles communication with card networks.

- Card Networks: Visa, MasterCard, American Express, etc.

1.3 Payment Gateway vs. Payment Processor

While often used interchangeably, a payment gateway facilitates the transmission of payment information, whereas a payment processor handles the actual transaction with banks and card networks.

2. How Payment Gateways Work

2.1 The Payment Flow

- Customer initiates checkout on an e-commerce site.

- Details are entered (credit card, PayPal, etc.).

- Data is encrypted and sent to the payment gateway.

- Gateway forwards data to the payment processor.

- Processor communicates with issuing bank/card network.

- Bank approves or declines transaction.

- Response is sent back through the gateway.

- Merchant confirms payment and fulfills order.

2.2 Transaction Types

- Authorization: Verifies funds, holds them temporarily.

- Capture: Transfers held funds to the merchant.

- Sale: Authorization + Capture in one.

- Refund: Returns funds to customer.

- Void: Cancels a pending authorization.

3. Integration Options for Developers

3.1 Hosted Payment Pages

- Simplest to implement.

- Redirects user to gateway page (e.g., PayPal Checkout).

- PCI burden is reduced.

3.2 Client-Side Integration

- Custom checkout with payment gateway’s JavaScript SDK (e.g., Stripe Elements).

- Sensitive data is tokenized in the browser.

3.3 Server-Side Integration

- Backend handles API calls.

- Offers complete control over the UI.

- Must ensure PCI compliance.

3.4 Hybrid Solutions

- Use JavaScript SDK + backend API calls.

- Balance between ease of integration and security.

4. Understanding APIs and SDKs

4.1 REST APIs

Most gateways offer RESTful APIs for managing transactions, customers, subscriptions, etc.

- Common endpoints:

- POST /charges

- GET /customers

- POST /refunds

4.2 SDKs

Official libraries often exist for popular languages:

- Node.js

- Python

- PHP

- Ruby

- Java

4.3 Webhooks

Used for asynchronous notifications:

- Payment success/failure

- Subscription renewals

- Dispute resolutions

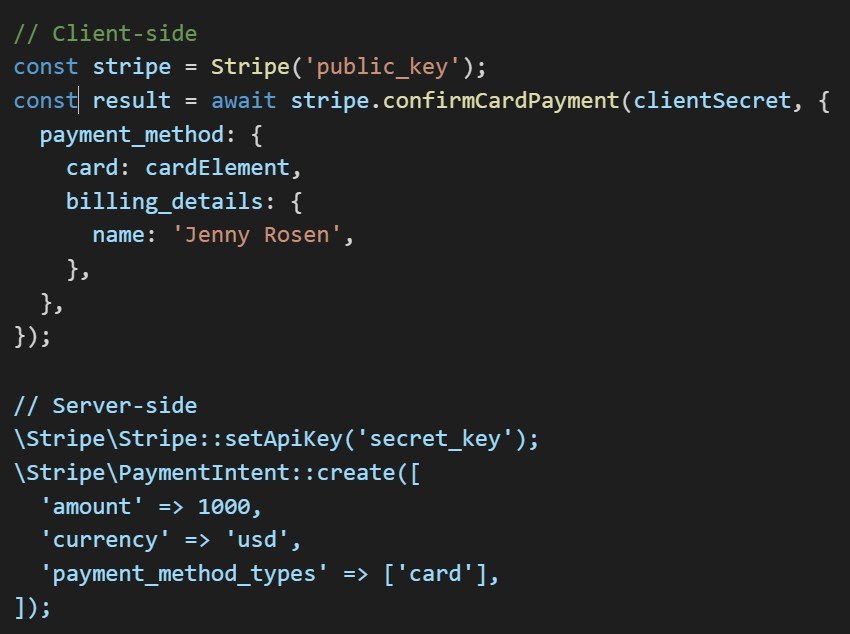

4.4 Example: Stripe API

5. Security Considerations

5.1 PCI-DSS Compliance

- Level 1 to 4 compliance based on transaction volume.

- Use of hosted fields and tokenization reduces PCI burden.

5.2 HTTPS Everywhere

- All payment data must be transmitted over TLS.

5.3 Tokenization

- Sensitive card data is replaced with a token.

- Token is meaningless if intercepted.

5.4 Data Encryption

- End-to-end encryption for all sensitive information.

5.5 3D Secure

- Additional authentication step for cardholders (e.g., OTP).

5.6 Fraud Detection Tools

- Machine learning models identify suspicious behavior.

- Velocity checks, geolocation, IP monitoring.

6. Compliance and Legal Obligations

6.1 PCI-DSS

- Global standard for secure card data handling.

- Mandatory for any merchant accepting cards.

6.2 GDPR

- Ensure user consent for data processing.

- Right to be forgotten, data portability.

6.3 PSD2 (Europe)

- Requires strong customer authentication (SCA).

- APIs for open banking.

6.4 KYC and AML

- Know Your Customer (KYC) for identity verification.

- Anti-Money Laundering (AML) laws to detect illegal activities.

7. Common Pitfalls in Payment Gateway Integration

7.1 Improper Error Handling

- Missing or misleading error messages can break user experience.

7.2 Not Using Webhooks

- Leads to missed updates (e.g., subscription renewals).

7.3 Storing Sensitive Data

- Never store CVV or full card numbers.

7.4 Ignoring Mobile Responsiveness

- Ensure checkout flows work seamlessly on mobile devices.

7.5 Poor UX Design

- A clunky checkout experience increases cart abandonment.

8. Testing and Deployment

8.1 Sandbox Environments

- Use gateway-provided test modes.

- Simulate successful and failed transactions.

8.2 Automated Tests

- Write unit and integration tests for payment flows.

8.3 Load Testing

- Ensure infrastructure can handle peak loads.

8.4 Monitoring and Logging

- Log every transaction and error.

- Use monitoring tools to detect downtime or unusual activity.

9. Comparing Popular Payment Gateways

9.1 Stripe

- Developer-friendly.

- Extensive API.

- Supports many currencies.

9.2 PayPal

- Trusted by users.

- Simple for small businesses.

- Higher fees than some competitors.

9.3 Square

- Great for in-person + online payments.

- Hardware and software integrations.

9.4 Braintree

- Owned by PayPal.

- Advanced fraud protection.

9.5 Adyen

- Enterprise-grade solution.

- Global support.

10. Advanced Features and Innovations

10.1 Recurring Billing

- Support for subscriptions, trials, and metered billing.

10.2 Split Payments

- Useful for marketplaces (e.g., paying vendors).

10.3 Real-Time Risk Analysis

- Adaptive fraud prevention.

10.4 Crypto Payments

- Accepting Bitcoin, Ethereum, and other tokens.

10.5 Buy Now, Pay Later (BNPL)

- Offer financing options with providers like Klarna, Affirm.

Conclusion

Payment gateways are the unsung heroes of the digital economy, enabling secure, smooth, and reliable transactions across the globe. For developers, understanding how they work and how to integrate them properly is crucial for delivering a seamless checkout experience and protecting customer data.

By following best practices in integration, security, and compliance, you not only reduce risk but also build trust with your users—a currency as valuable as any payment method. Whether you’re working with a hosted solution or building a custom payment flow, this guide gives you the foundation to do it right.